Available for banks and credit unions of all sizes.

Your clients want to invest.

They just aren’t doing it with you.

Today, less than 1% of Americans invest through their bank or credit union. The rest turn to third-party platforms — Betterment, Vanguard, Robinhood — that don’t just capture investment dollars. They actively promote high-yield savings accounts to pull deposits away from your institution.

Yet 53% of Americans say they’d prefer to invest with their trusted financial institution if the option existed. The gap between what members want and what most FIs offer is the opportunity — and the risk.

53% want to invest with you

vs

less than 1% do

The Solution

Bring investing inside your platform — not alongside it

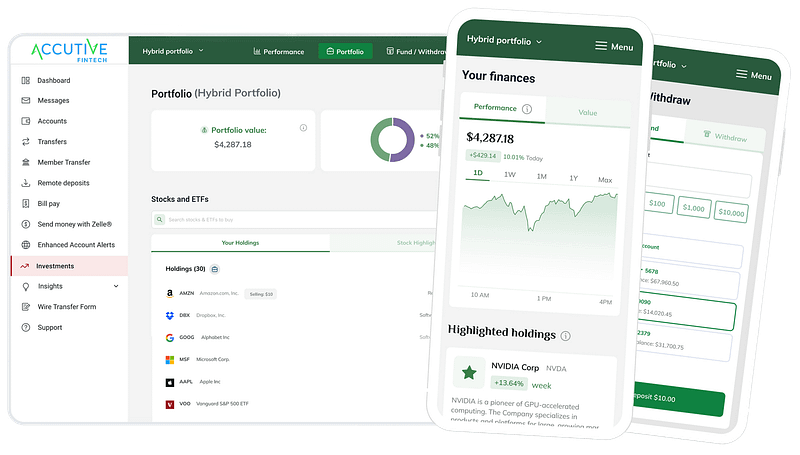

Eko is a white-label digital investment platform that Accutive FinTech deploys natively within your existing digital banking experience. Members never leave your app. Money moves instantly — no core dependency required. And your institution owns the experience, top to bottom. From pre-built robo portfolios to self-directed investing, IRAs, and crypto, Eko gives your members the full range of investment options they’re currently getting from Robinhood — delivered through a brand they already trust: yours.

Real results from real financial institutions — ranging from $70M to $15B in assets.

3.8x

More frequent logins from members who invest through Eko.

+11%

Average deposit growth after year one vs. flat for non-Eko members.

7%

Of your member base will fund an investment account in year one.

6x

Less likely to leave — Eko users vs. non-investing members.

$1,740

Average investment per member at 12 months (grows to $2,775 by year 2)

65%

Of Eko investors are

Millennials or Gen Z.

Based on outcomes across 8 Eko financial institution partners, ranging from $70M to $15B in assets, after 12+ months of deployment.

Six ways Eko changes the equation for your institution.

Keep Deposits In-House

Eko users grow their deposits by an average of 11% after year one — significantly outpacing members who invest elsewhere.

Boost Engagement & Stickiness

Investing members log in 3.8× more often. 30% log in more than 10 times per week — deepening your relationship at every touchpoint.

Retain Members Long-Term

Eko members are 6× less likely to leave your institution. When they invest with you, they stay with you.

Native Integration, No Core

Dependency

Eko lives inside your existing digital banking platform. No redirects. No separate app. Instant money movement without touching your core.

Attract the Next Generation

65% of Eko investors are Millennials or Gen Z — the demographic most likely to move their primary financial relationship to whoever offers the best digital experience.

Fully White-Labeled

Your brand. Your app. Your members invest through the interface they trust — Eko powers it invisibly behind the scenes.

Everything your members expect from a

modern investment platform — inside the app they already use.

Pre-Built Portfolios (Robo) — Members choose from professionally constructed portfolios based on their risk tolerance. No financial advisor required.

Self-Directed Investing — Buy and sell individual stocks, ETFs, and bonds directly within your banking app.

Hybrid Investing — A combination of robo guidance and self-directed control, giving members flexibility as their confidence grows.

IRA & Roth IRA Accounts — Tax-advantaged retirement accounts, offered natively through your platform.

Crypto — Optional crypto exposure for FIs that choose to enable it.

Start from $1 — No minimums to begin investing. Accessible to every member, not just high-net-worth clients.

Works natively with the digital

banking platforms you already run.

Eko integrates directly into major digital banking platforms — no custom middleware, no API rebuilds. If your members are already using one of these platforms, Eko can be live in weeks, not months.

Don’t see your platform? Contact us — Eko’s flexible architecture is built for new integrations.

Built for banks. Built for credit unions.

Eko is designed for the full range of financial institutions — from $70M community credit unions to $15B regional banks. The platform adapts to your member base, your brand, and your digital banking environment.

FOR BANKS

The problem

Less than 1% of your customers invest with you. Betterment, Vanguard, and Robinhood are actively targeting them with high-yield savings accounts designed to pull deposits away.

The Eko advantage

Offer the digital investment experience your customers expect — without building it. White-labeled, natively embedded, and up in weeks.

Case study range

Deployed with banks from $100M to $15B in assets (Union Bank, Mercantile Bank Corporation, Lake City Bank, Bell Bank).

Investment apps aren’t just competing for investment dollars -they’re competing for your members’ primary financial relationship. Once a member moves money out, the relationship erodes.

The Eko advantage

Turn your cooperative trust model into a competitive advantage. When members invest through you, they’re 6× less likely to leave — and deposit growth accelerates.

Case study range

Deployed with credit unions from $70M to $5B in assets (Educators Credit Union, Brooklyn Cooperative, Eagle Community CU, Carter Credit Union).

Ready to see what Eko looks like inside your platform?

Book a demo with our team. We’ll show you Eko running natively inside a banking environment — and walk through the deployment path for your institution’s specific setup.